In March 2026, U.S. clean electricity outgenerated fossil fuels for the first time. The milestone matters. But the deeper story is about storage, grid bottlenecks, rising demand, and whether climate tech can win not just a month, but the next decade.

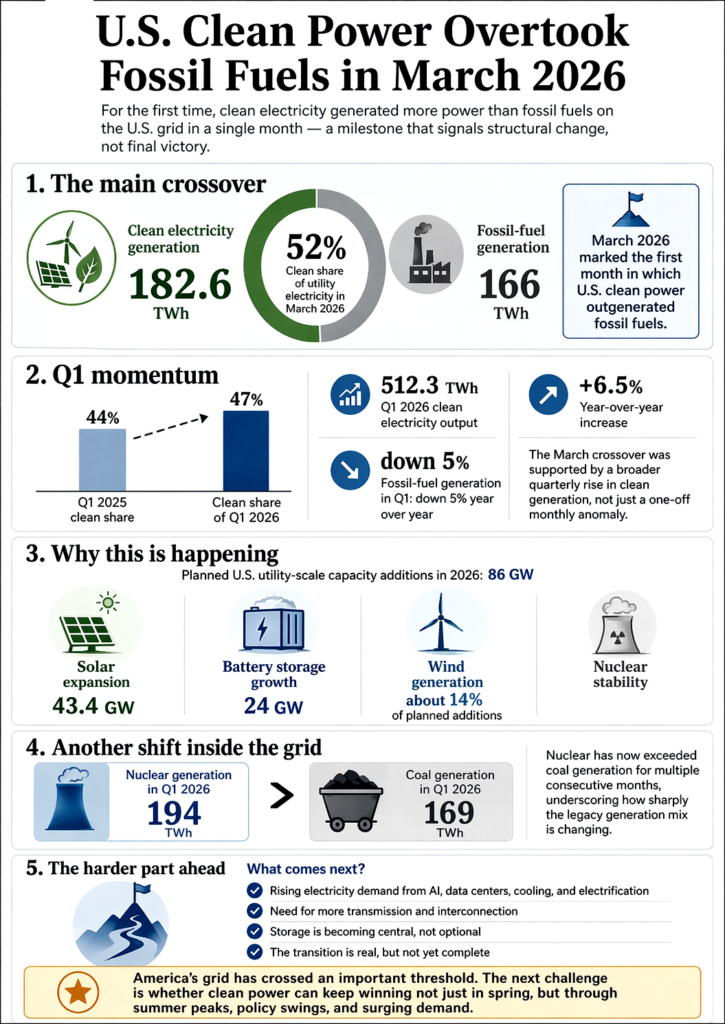

In March 2026, something quietly historic happened on the U.S. grid. Clean power sources — renewables plus nuclear — generated 182.6 terawatt-hours of electricity, more than the 166 TWh produced by fossil-fuel plants. That gave clean sources 52% of utility electricity for the month, the first time they have moved ahead of fossil generation in Ember’s monthly data for the United States.

The striking part is not only the crossover itself. It is that it arrived while Washington was moving in the other direction. The U.S. power system kept setting clean-energy milestones even after the Trump administration cut support for renewables and backed more fossil-fuel output. In the first quarter, clean electricity output reached a record 512.3 TWh, up 6.5% from a year earlier, while fossil-fuel generation fell 5%; clean sources supplied 47% of electricity in the quarter, up from 44% in Q1 2025.

Still, March should not be mistaken for a finish line. Spring is favorable to wind, summer has not yet forced the grid into its most air-conditioning-heavy hours, and solar has not yet reached its seasonal peak. EIA still expects renewables to account for about 25% of U.S. electricity generation in 2026, with nuclear holding at 18%, which implies that the country is not yet operating a majority-clean grid on an annual basis. The milestone is real, but it is directional before it is permanent.

A monthly record backed by a structural build-out

That distinction matters because it helps separate symbolism from system change. If March were only a weather story, it would be interesting and forgettable. It is not. The data says the U.S. is building the physical base of a cleaner grid at unusual speed. Developers plan to add a record 86 GW of utility-scale generating capacity in 2026 if scheduled projects are completed: 43.4 GW of solar, 24 GW of battery storage, and roughly 14% of additions from wind. In 2025, the grid added 53 GW of capacity, the largest annual installation total since 2002.

That is why this is best understood as a climate-tech story rather than a simple policy story. The center of gravity is shifting from standalone renewable generation to integrated systems: solar plus storage, wind plus better forecasting, batteries plus software, nuclear plus uprates, and increasingly a grid that treats flexibility as a resource rather than a backup plan. EIA expects utility-scale solar generation to climb from 290 billion kWh in 2025 to 424 billion kWh by 2027, while renewable-led growth drives total U.S. electricity generation higher in both 2026 and 2027.

The U.S. milestone also fits a broader pattern. Ember’s Global Electricity Review 2026 says clean electricity growth was large enough to meet all additional electricity demand worldwide in 2025, while the IEA says renewables accounted for the vast majority of global generation growth and that fossil-fuel electricity declined. America’s March crossover was not a self-contained national curiosity. It was a local signal within a wider global reordering of power economics.

Storage is becoming the technology that changes the argument

Solar’s rise by itself is not new. What is new is how batteries are changing solar’s role on the grid. EIA says U.S. battery storage capacity has grown by more than 40 GW over the past five years, and developers plan another 24 GW in 2026 after a record 15 GW was added in 2025. In ERCOT, battery capacity is expected to expand from about 15 GW in 2025 to 37 GW by the end of 2027, a build-out that matters because it turns cheap midday solar into something closer to dispatchable evening power.

California already offers a glimpse of what that looks like in practice. Batteries were CAISO’s single largest source of electricity between 7 p.m. and 9 p.m. on June 19, 2025, supplying roughly 26% of total power during that period, ahead of natural gas. That does not mean gas is gone. It does mean the old claim that renewables are inherently too intermittent to play a central grid role is becoming harder to defend in markets where storage is scaling.

Coal is slipping, but the transition is not linear

Another important detail in the March data is that nuclear has quietly started to matter more in the public story. Nuclear output has exceeded coal-fired generation for eight straight months, the longest such stretch on record. In the first quarter, nuclear reactors generated 194 TWh, ahead of coal at 169 TWh, while coal-fired emissions fell to about 177 million metric tons, below the roughly 219 million-ton average for the same period over the previous three years.

But the fossil side of the grid is not retreating cleanly. EIA says only 2.6 GW of coal-fired capacity retired in 2025, the least since 2010, after multiple planned closures were delayed or canceled. Another 6.4 GW of coal capacity is scheduled to retire in 2026, but EIA has already warned that emergency orders and reliability concerns can keep aging plants online longer than planned. That is a useful corrective to triumphal narratives: output is shifting faster than the physical retirement of the legacy fleet.

The harder race is against load growth, not ideology

The biggest test of all may be demand. According to EIA, U.S. electricity consumption hit a record 4,195 billion kWh in 2025 and is expected to rise again in 2026 and 2027, driven in large part by AI and crypto data centers, as well as wider electrification in homes, business, and transport. EIA also expects residential and commercial power demand this summer to rise about 3% from last year as cooling needs increase. Clean power is not replacing a static fossil system; it is trying to outrun a grid that keeps getting hungrier.

That is why the real climate-tech challenge has shifted. For years the question was whether clean energy could become cost-competitive and scale. In many markets, it plainly has. In 2025 the utility-scale solar paired with batteries was already cost-competitive with new gas peakers in Lazard’s analysis, while the IEA says utility-scale solar remains the cheapest source of new electricity generation in most parts of the world. The harder question now is whether the clean system can be assembled quickly enough — with storage, flexible demand, transmission, and market rules included — to keep pace with load growth.

The pipeline is huge. The grid is the bottleneck.

The interconnection queue shows why this next phase is more about systems engineering than technological invention. Lawrence Berkeley National Laboratory says that at the end of 2024, around 10,300 projects were actively seeking grid interconnection in the U.S., representing about 1,400 GW of generation and roughly 890 GW of storage. That is an extraordinary backlog of ambition. It also means the country’s biggest clean-power constraint is increasingly not whether developers want to build. It is whether the grid can connect, transmit, and absorb what they are trying to build.

This is where March’s milestone becomes more than a good headline. It suggests that the U.S. power system is no longer merely testing climate tech around the edges. It is beginning to run on it. But the next phase will not be won by adding solar modules alone or by declaring victory after one spring month. It will be won by making the system itself more operable: faster interconnection, more transmission, more storage duration, smarter demand response, better forecasting, and in some cases more output from the nuclear fleet that is already on the ground. The DOE’s new UPRISE program, which targets 5 GW of additional nuclear capacity by 2029 through uprates and restarts, is one sign that policymakers are starting to think in that systems language too.

So the March crossover deserves attention, but not sentimentality. It was not the month America solved the grid. It was the month the grid made a harder fact visible: clean electricity is no longer a peripheral supplement that needs perfect politics to survive. It is becoming the default growth engine of the power system. The real question now is whether the country can build the wires, storage, flexibility, and market design needed to make that advantage hold through summer peaks, policy swings, and the next surge in demand. That is not a softer question than whether solar works. It is the more consequential one.