Europe has spent decades perfecting a particular kind of power: writing rules that others eventually adopt—on chemicals, privacy, product standards, and carbon. This week, it tried something more muscular and more market-facing: using public money to create “lead markets” for low-carbon materials and European-made clean tech.

On March 4, the European Commission unveiled the Industrial Accelerator Act (IAA)—a legislative proposal that reads like a memo from an anxious boardroom: Europe’s manufacturing base is shrinking, its clean-tech supply chains are heavily exposed, and the cost of industrial decarbonization is rising just as geopolitical risk is rewriting the price of energy, resilience, and dependency.

The Commission’s headline goal is blunt: raise manufacturing from 14.3% of EU GDP (2024) to 20% by 2035. In other words, reverse a 25-year slide and do it while cutting emissions. The bet is that the climate transition won’t survive politically—or practically—if it looks like Europe is only importing the future.

What’s new isn’t industrial policy. The novelty is the doctrine shift: from “the market will sort it out” to “public procurement and subsidies will tilt the playing field.” Europe is trying to become the buyer that makes low-carbon steel, low-carbon cement, and EU-made batteries bankable—not just “nice to have.”

The uncomfortable math behind the pivot

Start with the numbers the Commission itself puts on the table:

- Manufacturing accounted for 14.3% of EU GDP in 2024, down from 17.4% in 2000.

- The sector is 18.3% of employment in the EU business economy and generates 26.2% of EU greenhouse-gas emissions—meaning decarbonizing industry is not optional if the EU’s climate targets are serious.

- The “strategic sectors” targeted by the IAA—energy-intensive industries, net-zero technologies manufacturing, and parts of the automotive ecosystem—are only about 15% of EU manufacturing production, but they sit upstream of everything that matters: construction, mobility, energy systems, and even defense.

This is the paradox Europe is trying to manage: the sectors that can unlock a cleaner economy are the same ones most exposed to cost pressure and import competition.

And then there’s the supply-chain reality check. The Commission argues that production of net-zero technologies is highly concentrated, with China accounting for over 80% of global battery manufacturing capacity and solar PV (including inverters). Whether or not every percentage point is debated, the direction is not: Europe’s clean transition is deeply linked to supply chains it doesn’t control.

What the Industrial Accelerator Act actually does

The IAA is designed around four levers that try to move the same object from different angles: demand, investment quality, permitting speed, and industrial clustering.

1) Demand-side “lead markets”: procurement and subsidies get rules

The core mechanism is simple: if public money is involved—through public procurement or certain public support schemes—then products must increasingly meet low-carbon and/or Union-origin (“Made in EU”) requirements.

A few specifics matter because they reveal the Commission’s philosophy: start targeted, and build optionality (and escape valves) into the system.

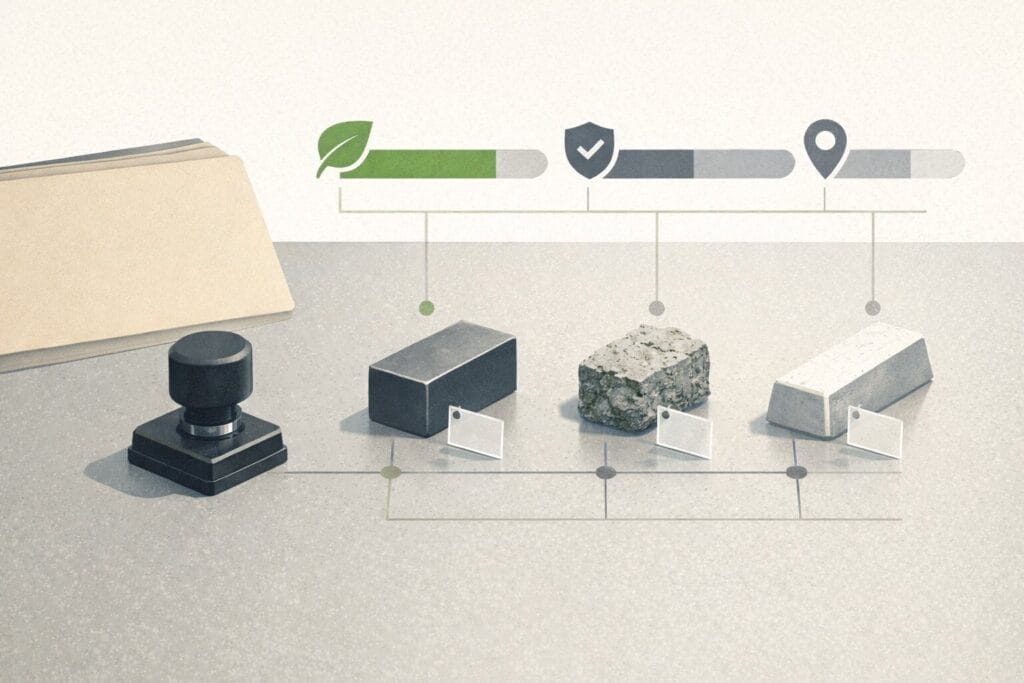

Low-carbon materials in public spending (from 2029):

Beginning January 1, 2029, public procurement and certain public support schemes tied to buildings, infrastructure, and civil motor vehicles would require minimum shares of low-carbon materials. The initial thresholds are not maximalist—they are “get the market moving” numbers:

- Steel: at least 25% of the total volume used must be low-carbon (notably, this is not explicitly tied to EU origin in the annex language).

- Concrete and mortar: at least 5% must be low-carbon and of Union origin (including clinker and cement used to produce them).

- Aluminium: at least 25% must be low-carbon and of Union origin.

Think of these as floor mandates meant to create price signals for producers who invest early in cleaner processes.

EV procurement and support: “70% EU components (ex-battery)” and more:

For publicly procured EVs (and EVs supported via certain schemes), the annexes go further into “what counts as made here.”

The baseline requirements include:

- The vehicle is assembled within the Union, and

- At least 70% of the ex-works price of vehicle components (excluding the battery) originates in the Union.

Then the rules reach into the battery and power electronics: requirements for additional battery components, e-powertrain components, and main electronic systems tighten over time (some kick in three years after entry into force).

This is industrial policy in its most literal form: a procurement rule that tells manufacturers what their bill of materials should look like.

2) “Reciprocity” and market access: openness becomes conditional

The Commission is careful to say the EU remains open. But it’s also clear the era of unconditional openness is ending—at least in strategic procurement.

The proposal explicitly leans on reciprocity: partners can be treated on par in procurement if they offer EU firms comparable access, including through frameworks like the WTO Government Procurement Agreement.

This is where “Buy EU” becomes less slogan and more negotiating tool. The EU isn’t just trying to buy European—it’s trying to trade procurement access for procurement access.

3) Foreign investment contribution: fewer “screwdriver plants,” more value capture

The third lever targets a specific fear: that Europe will attract “investment” that amounts to assembly operations using imported components, with limited local jobs and minimal technology transfer.

Under the Commission’s framing, certain large foreign investments in strategic sectors would face conditions—particularly investments of €100 million or more by companies from non-EU countries that control more than 40% of global manufacturing capacity in relevant areas (the Commission signals this is largely about China in practice).

The factsheet makes the intent explicit: ensure such investments generate maximum added value in the EU, with requirements including at least 50% employment of Union workers, plus expectations around local content, ownership, technology/knowledge transfer, and R&D activities.

This is a different kind of investment screening—not just “is it a national security risk?” but “does it build European capability?”

4) Permitting and industrial “acceleration areas”: make speed a policy tool

Even supporters of local content rules tend to agree on one point: Europe’s permitting and project timelines can kill industrial momentum faster than any competitor.

The Commission’s response is to standardize and digitize permitting workflows—“one project, one digital procedure”—and push member states to create Industrial Acceleration Areas, where projects can move faster through streamlined, area-wide permitting logic.

The intent is to make industrial decarbonization projects feel less like bespoke bureaucratic adventures and more like repeatable deployment.

The fine print that will decide whether this becomes real—or symbolic

The IAA’s political genius may be that it sounds decisive while leaving itself room to breathe. Its practical risk is the same: too many escape hatches can turn a mandate into a suggestion.

One of the clearest examples is how procurement origin requirements can be waived. The proposal includes carve-outs where authorities may decide not to apply one or more requirements—if there’s only one viable supplier, if suitable tenders don’t materialize, if costs would be disproportionate, or if delays would be significant. The text even signals thresholds: cost differences above 25% may be presumed disproportionate, and delivery delays exceeding seven months may be presumed significant.

That’s not trivial. Low-carbon materials often are more expensive today. If “25% extra cost” becomes the default argument, then Europe may discover it has written a rule that politely steps aside whenever it gets uncomfortable.

Will “Buy EU” accelerate decarbonization—or slow it down?

Here’s the tension the Commission is trying to balance, and it’s the same one every climate-industrial policy eventually hits:

You can’t build clean supply chains without demand certainty.

But you also can’t decarbonize fast if the rules make clean tech and clean materials more expensive and harder to procure.

Supporters argue procurement is precisely the right lever because it’s enormous. Reuters cites EU public procurement at more than €2 trillion—about 14% of EU economic output—a scale large enough to create “lead markets” without passing a new consumer tax.

Critics—and some market analysts—warn that aggressive local-content rules can raise costs and complicate supply chains, potentially undermining both competitiveness and near-term emissions trajectories. Even within the EU, member states disagree on how narrow or broad the “trusted partner” list should be—an early sign that implementation could become a political tug of war.

The ClimateTech angle: a new market for “proof”

Even if you ignore the geopolitics, the IAA quietly expands something ClimateTech companies increasingly sell: verification.

If governments must buy low-carbon steel (and prove it), you need:

- carbon intensity methodologies,

- auditable product data,

- traceable bills of materials,

- reliable declarations for “Union origin,” and

- tooling that procurement officers can actually use.

In other words: industrial decarbonization isn’t just about making cleaner stuff—it’s about proving it at scale. That creates a second-order market for MRV (measurement, reporting, verification), digital product passports, supply-chain traceability, and procurement compliance infrastructure.

Europe is not just trying to manufacture more. It’s trying to manufacture credibility—in carbon claims, in supply security, and in the political durability of the transition.

What to watch next

- Definitions that bite: How the EU ultimately defines “low-carbon” by product category will decide whether the policy accelerates investment—or triggers endless disputes.

- The partner list: “Trusted partners” sounds diplomatic. In practice, it’s a map of who Europe believes will share industrial risk—and who it believes might exploit its market.

- The escape hatches: If 25% cost premiums and seven-month delays become routine, the mandates could be diluted before they matter.

- Permitting reforms as the real story: If the IAA meaningfully reduces project cycle times, it may do more for industrial decarbonization than the procurement quotas themselves.

Bottom line

The Industrial Accelerator Act is Europe’s attempt to answer a question it has avoided for years: Can a climate transition survive if it deindustrializes the place trying to lead it?

The Commission’s answer is to use the state not just as regulator, but as customer—and to treat supply chains as a strategic asset, not a background assumption.

Whether this becomes a genuine acceleration or a carefully branded compromise will depend less on the headline targets and more on the operational details: how strict the definitions are, how political the partner list becomes, and how often the exceptions get used.

Europe is trying to buy its way into resilience. The world—and Europe’s own industries—will now test the price.